|

|

SCAN Health Plan Achieves

Milestone, Serving More Than 200,000 Members in California & Achieving a

90% Satisfaction Rating

|

|

Looks

like SCAN is doing things right. The not-for-profit Medicare Advantage

provider announced that it has surpassed the 200,000 membership mark in

California, representing a near 20 percent five-year increase. SCAN has

maintained for two years in a row its 4.5-star rating out of a possible five

stars from the Centers for Medicare and Medicaid Services (CMS).

SCAN

was also named one of the best insurance companies for Medicare Advantage for

2019 by U.S. News & World Report, and received a 90 percent member satisfaction rating

as reported in the 2019 Medicare & You Handbook.

What

is SCAN Health Plan?

SCAN

Health Plan is a not-for-profit, Medicare Advantage (Part C), health

maintenance organization based in Long Beach, California. Founded in 1977,

they provide healthcare coverage to Medicare beneficiaries throughout

California.

Medicare

Advantage Plans, sometimes called "Part C" or "MA Plans,"

are an “all in one” alternative to Original Medicare. They are offered by

private companies approved by Medicare. If you join a Medicare Advantage

Plan, you still have Medicare. These "bundled" plans include

Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance),

and usually Medicare prescription drug (Part D).

Interested

in SCAN or know someone who is?

If

you, or someone you know, is interested in enrolling in SCAN, or need help

navigating through the confusing path of medicare - please feel free to give

us at Ample Insurance Services a call. All calls and consultations are free.

We also offer other companies besides SCAN as well, such as Blue Cross, Blue

Shield, Aetna, and more.

Connect

with us today -

(909)

746-9127

|

Friday, February 8, 2019

SCAN Rated One of the Best Medicare Companies for 2019

Thursday, January 31, 2019

Important Opioid Information for Medicare Members

|

|

|

Wednesday, January 30, 2019

Tired of Dealing with Insurance Agents?

We get it, insurance agents can be annoying. And maybe you prefer to do things on your own. Good news, simply click the images below to instantly quote & apply with the various insurance companies we're affiliated with. No agent nor consultation required. Stress free, risk free, and quick!

Don't see what you're looking for? It probably requires us to submit an application or get the quote for you. Simply call, text or email us (909) 746-9127 // info@aacefs.com with what you're looking for. We promise to be quick and treat you like a human, not a sale.

| |||||||||||||||||||

When Drivers Should Check Other Car Insurance Quotes

When it comes to the premium drivers pay on their car insurance, certain events can affect the amount they pay. Whether if those events affect their car insurance rates in a positive or negative way, drivers can find out by checking the car insurance market at least once every six months.

Drivers are recommended to check the online insurance market in the following situations:

- Driver's credit score changed. Insurance companies are allowed to take drivers credit score into consideration when determining their premium rates. Drivers with a good score will pay less, while drivers with bad credit score will pay more on their premium rates.

- State's laws have changed. The car insurance laws and the requirements are different in each state. These laws and requirements can change at any time, so it's important for the policyholders to be vigilant.

- Driver's has maintained coverage. If the policyholder is a new driver or a more experienced driver that has a coverage lapse, then the policyholder is considered a high-risk driver. High-risk drivers pay more on their premiums, and in order to get rid of the high-risk label, they need to maintain coverage for at least six months.

- Major life events. Several events that happen in the life of a policyholder can affect their premiums. Events, like getting married, moving to a low-crime neighborhood, or buying a safer car, can make the policyholder premium rates to decrease. Events, like getting divorced, moving to a high-crime neighborhood, or buying an unsafe vehicle, will make the policyholder premium to increase.

- Policy renewal time is getting closer. This the best time for a policyholder to shop for online quotes. Many rival insurance companies will try to lure the policyholder to their companies, by offering him all sorts of discounts and offers.

Monday, January 28, 2019

Cheap Business Insurance in Chino Hills!

Contact us today - we're not tied down to one company and will shop for you to find your business the best rate!

855-480-2223 (Toll Free)

909-746-9127 (Call/Text)

info@aacefs.com

Friday, January 25, 2019

Thursday, January 24, 2019

Wednesday, January 23, 2019

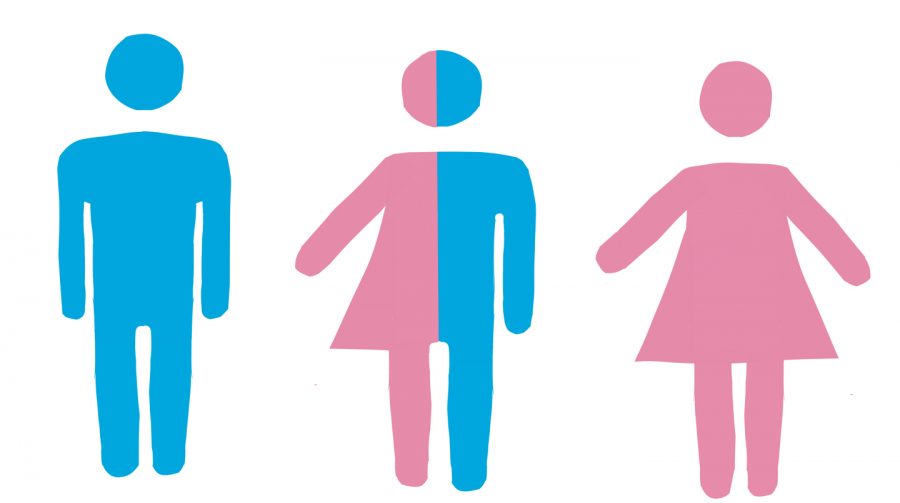

NEW CALIFORNIA LAW - Gender Can No Longer Be Considered in Setting Car Insurance Rates

California joined about a half-dozen states this month in banning the use of a person’s gender when assessing risk factors for car insurance, a change that could potentially alter rates for scores of drivers across the state.

The state, which is the country’s most populous, requires insurers to prioritize criteria like drivers’ safety records and years of experience behind the wheel when setting auto rates, but it also allows them to weigh other factors, like marital status. Gender had been among the optional criteria until the beginning of this year, when a new regulation went into effect prohibiting the practice.

In announcing the change, the departing state insurance commissioner, Dave Jones, said the new regulations “ensure that auto insurance rates are based on factors within a driver’s control, rather than personal characteristics over which drivers have no control.”

Mr. Jones’s term as commissioner ended in early January, and the new regulation was one of his final acts. The state’s Insurance Department, in explaining its reasoning for the change, noted that the industry had inconsistently — and perhaps unfairly — applied gender weighting in pricing.

Some insurers found that female drivers were a higher risk while others claimed the inverse, the department concluded, and the factoring of gender on rates varied widely by location.

“Gender’s relationship to risk of loss no longer appears to be substantial,” the department noted, saying the rationale for using it was “suspect.”

“Charging drivers different rates by their gender might have seemed like a good idea decades ago,” Ricardo Lara, the new state insurance commissioner, said in an emailed statement. “Gender, race, ethnicity or sexual orientation are beyond your control, and it is not a fair or even an effective way to predict risk.”

The specific impact on someone’s insurance rates in California remains uncertain. Insurers have until at least July to submit gender-neutral auto rating plans to the Insurance Department for review.

Removing the gender factor could in effect equalize rates for inexperienced drivers: Younger men, who have typically paid higher rates, on average might see declines, while younger women could see increases. In an economic analysis of the change, the Insurance Department estimated that female drivers with three or fewer years of driving experience were expected to see the biggest impact, with rates going up 6 percent on average. Male drivers with similar driving experience could have a corresponding decrease of about 5 percent.

The department’s analysis, based on 17 companies that make up about two-thirds of the state’s consumer car insurance market, estimated scant effect on rates over all.

The impact for any given driver, however, could “vary considerably” by the individual, by the insurer and by the type of coverage chosen, the state noted.

Janet Ruiz, a spokeswoman for the Insurance Information Institute, an industry group, said she didn’t expect California drivers over all to see a big impact on premiums, because gender wasn’t one of the top factors used in setting rates anyway.

Other states that ban the use of gender in setting rates include Hawaii, Massachusetts, Montana, North Carolina and Pennsylvania, according to the Consumer Federation of America, a nonprofit advocacy group. Most other states allow the practice, and insurers have long argued that the use of gender in setting premiums is sound actuarial practice.

The rule change in California followed the advent of a state law aimed at accommodating the concerns of transgender people when using identity documents. The Gender Recognition Act of 2017 in part allows Californians to choose, in addition to “male” or “female,” a third category of “nonbinary” on their state driver’s licenses. The law describes nonbinary as an umbrella term for people whose gender identities “fall somewhere outside of the traditional conceptions of strictly either female or male.” The option became available Jan. 1.

In Oregon, where drivers may select “not specified” as a third gender category on their licenses, insurers may continue to use gender as a factor in setting rates. However, insurers must submit documentation justifying how they rate those drivers.

Here are some questions and answers about auto insurance premiums:

What factors do insurers consider when setting auto insurance rates?

The rules vary by state, and some exclude or restrict certain criteria. Typical factors used by insurers to assess a driver’s risk and set premiums, in addition to your driving record and claims history, might include where you live, your age, education, occupation, marital status, credit history and the type of car you drive, according to the National Association of Insurance Commissioners.

What can I do if I think my auto premium is too high?

Industry representatives and consumer advocates alike advise people to seek quotes periodically from competing insurers. Contact us at Ample Insurance Services for free quotes from over 8+ auto insurance companies.We do the work for you, free of charge.

What else can I do to keep my auto rates affordable?

Consider raising your deductible, the amount subtracted from your check when an insurer pays a claim under your policy. Going from $500 to $1,000 can save between 10 and 15 percent annually on premiums. Also, make sure you don’t let your policy lapse; if you go without coverage even for a day, you’ll likely see your rates rise. And, she said, bundling your coverage for renter’s or homeowner’s insurance with your auto policy with the same insurer can save an average of 8 percent annually.

Tuesday, January 22, 2019

Friday, January 11, 2019

Presentation in Chino Hills

We were happy to present our products today at the weekly CRMLS meeting in Chino Hills, CA.

Please contact us today if you'd like more information.

855-480-2223 / info@aacefs.com

Thursday, January 10, 2019

Subscribe to:

Comments (Atom)

SCAN Rated One of the Best Medicare Companies for 2019

SCAN Health Plan Achieves Milestone, Serving More Than 200,000 Members in California & Achieving a 90% Satis...

-

Feel confident saying YES! to all adventures life has to offer by protecting yourself with disability and/or accident insurance. How coul...

Feel confident saying YES! to all adventures life has to offer by protecting yourself with disability and/or accident insurance. How coul... -

There are more than 28,000 claims for residential personal property, nearly 2,000 from commercial property and 9,400 in auto and other clai...

There are more than 28,000 claims for residential personal property, nearly 2,000 from commercial property and 9,400 in auto and other clai...